Cash flow is the lifeblood of any trucking business. Between rising fuel costs, unpredictable maintenance expenses, and brokers who take 30, 60, or even 90 days to pay, many trucking companies find themselves in a constant cash crunch.

When you need working capital, two common solutions emerge: freight factoring and bank loans. But which one is right for your business?

In this guide, we’ll break down:

✔ How freight factoring works (and when it makes sense)

✔ The pros and cons of traditional bank loans

✔ Key differences in cost, speed, and flexibility

✔ Real-world scenarios to help you decide

By the end, you’ll know exactly which financing option—or combination—will keep your trucks rolling and your business growing.

Freight Factoring: Instant Cash for Your Invoices

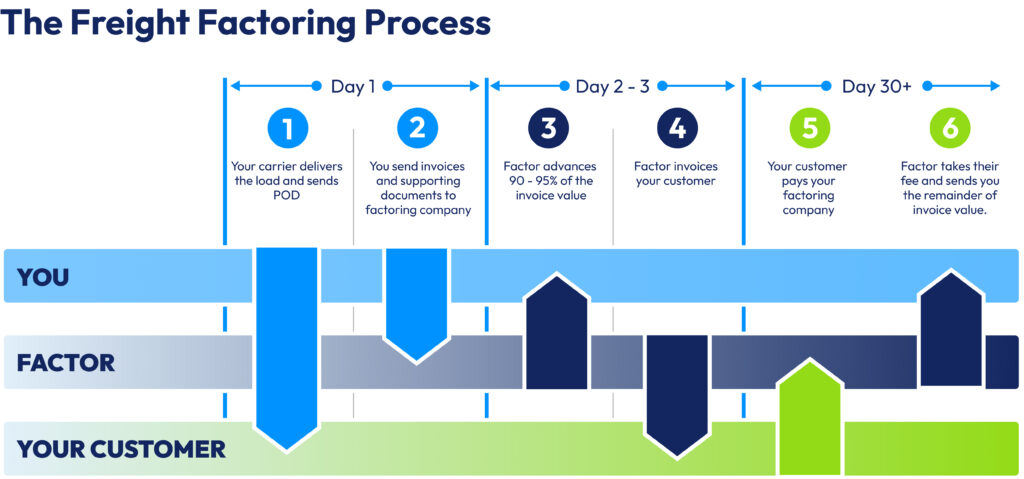

How It Works

Freight factoring is simple:

- You complete a load and invoice the broker/shipper.

- You sell that unpaid invoice to a factoring company.

- They advance you 80-95% of the invoice value (usually within 24 hours).

- They collect payment from your customer and send you the remaining balance (minus their fee).

Biggest Advantages

✅ Fast funding – Get cash in your account within 1-2 days, not weeks.

✅ No credit check (on you) – Approval depends on your customer’s credit, not yours.

✅ No long-term debt – Unlike loans, factoring isn’t a liability on your balance sheet.

✅ Scales with your business – More loads = More available cash.

Potential Drawbacks

❌ Higher cost than loans – Factoring fees range from 1-5% per invoice, which adds up over time.

❌ Customer interactions – Some factoring companies handle collections aggressively, which could strain broker relationships.

❌ Dependency risk – Once you rely on factoring, transitioning away can be tough.

Who Should Use Factoring?

✔ Newer trucking companies (banks won’t lend to you yet)

✔ Owner-operators needing quick cash for fuel, repairs, or payroll

✔ Businesses with slow-paying customers (30+ day terms)

Bank Loans: Lower Cost, But Harder to Get

How It Works

A bank loan provides a lump sum of cash upfront, which you repay (plus interest) over a set term.

Biggest Advantages

✅ Lower interest rates – Typically 5-10% APR, cheaper than factoring long-term.

✅ Keep customer relationships – No third party contacting your brokers.

✅ Good for big investments – Buying trucks, hiring drivers, or expanding operations.

Potential Drawbacks

❌ Strict approval requirements – Banks want strong credit, steady revenue, and often collateral (like your truck).

❌ Slow funding – Approval can take weeks or even months.

❌ Debt burden – Loans appear on your balance sheet, affecting future borrowing.

Who Should Get a Bank Loan?

✔ Established fleets with good credit and financials

✔ Companies making large purchases (equipment, expansion)

✔ Businesses that want predictable monthly payments

Key Differences: Factoring vs. Bank Loans

| Feature | Freight Factoring | Bank Loan |

|---|---|---|

| Speed | 1-2 days | Weeks to months |

| Credit Check | Based on customer credit | Based on your credit |

| Cost | 1-5% per invoice | 5-10% APR |

| Debt | No | Yes |

| Best For | Short-term cash flow | Long-term investments |

Real-World Scenarios: Which One Wins?

Scenario 1: Emergency Repair

- Problem: Your truck breaks down, and you need $5,000 fast to get back on the road.

- Solution: Factoring – Get cash in 24 hours without a credit check.

Scenario 2: Buying a Second Truck

- Problem: You want to expand but need $100,000 for a new rig.

- Solution: Bank loan – Lower interest rates make it cheaper over 5+ years.

Scenario 3: Seasonal Slowdown

- Problem: Winter freight volume drops, but bills keep coming.

- Solution: Factoring – Cover gaps without taking on long-term debt.

Can You Use Both?

Absolutely! Many successful trucking companies combine both strategies:

✔ Use factoring for day-to-day cash flow.

✔ Take out a bank loan for major purchases.

Just be careful not to over-leverage your business.

Final Verdict: Which One Should You Choose?

Freight Factoring is Best If You Need:

✔ Fast cash (within days)

✔ No credit check

✔ Flexibility (no long-term commitment)

Bank Loans Are Better If You Have:

✔ Strong credit & financials

✔ Time to wait for approval

✔ A big, planned expense

Next Steps

- Calculate your costs – Compare factoring fees vs. loan interest.

- Check your credit – If it’s strong, a loan may save you money.

- Talk to lenders – Get pre-approved rates before deciding.

Need help choosing? Drop a comment—we’ll help you crunch the numbers! 🚛💰

Bottom Line

There’s no “perfect” financing option—just the right one for your situation. Whether you choose factoring for speed or a loan for stability, the key is making an informed decision that keeps your business moving forward.

Now, go hit the road—and keep that cash flowing!